Author: Yong

Bio-innovative drugs are emerging industries in the pharmaceutical industry, and the national “Twelfth Five-Year Plan†has identified the focus of biomedical development. Polypeptide drugs due to broad indications, safety and efficacy of notable features, has been widely used in the prevention, diagnosis and treatment of diseases of cancer, hepatitis, diabetes, AIDS, has broad development prospects. Antibody - drug conjugates (ADC) in conjunction with highly cytotoxic drugs and small molecule drugs targeting monoclonal antibodies, can effectively kill tumor cells in preclinical studies, and even human clinical studies, and achieved good anti-tumor The effect has become one of the hot areas of biopharmaceutical research.

First, peptide drugs

A polypeptide is a compound formed by a plurality of amino acids joined by peptide bonds, usually composed of 10-100 amino acid molecules, which are linked in the same manner as proteins, and have a relative molecular mass of less than 10,000. Polypeptides are ubiquitous in organisms. To date, tens of thousands of peptides have been found in organisms. They widely participate in and regulate the functional activities of various systems, organs, tissues and cells in the body, and play an important role in life activities. The preparation of peptide drugs currently has three methods of chemical synthesis, genetic recombination and extraction from plants and animals. The production of solid phase synthesis technology in chemical synthesis has greatly promoted the development of peptide drugs. Gene recombination refers to the process of forming new DNA molecules by the exchange and recombination of DNA fragments due to the cleavage and ligation of different DNA strands. Gene recombination is mainly used in the preparation of long peptides in polypeptide drugs. According to statistics, in 2012, there were 128 peptide drugs entering clinical research, including 40 in phase I clinical research, 74 in phase II, and 14 in phase III.

Internationally, peptide drugs are mainly used in the fields of chronic diseases, tumors and rare diseases, and there are many heavy varieties. As the patents for multiple peptide varieties expire, peptide generics will usher in development opportunities, and upstream peptide drug manufacturers will also benefit from the growth of the generics market. At present, the global market for peptide drugs has exceeded 20 billion US dollars, accounting for about 2% of the total market share of pharmaceutical products, maintaining a growth rate of about 10%. Internationally, heavy peptide drugs are mainly concentrated in the fields of tumors, chronic diseases and rare diseases, while the peptide drugs in China are mainly used for immune assist and gastrointestinal hemostasis, such as thymopentin and somatostatin. With the expiration of patents for multiple peptide heavy products, generic drugs will have an opportunity.

1.1 The current status of the global market

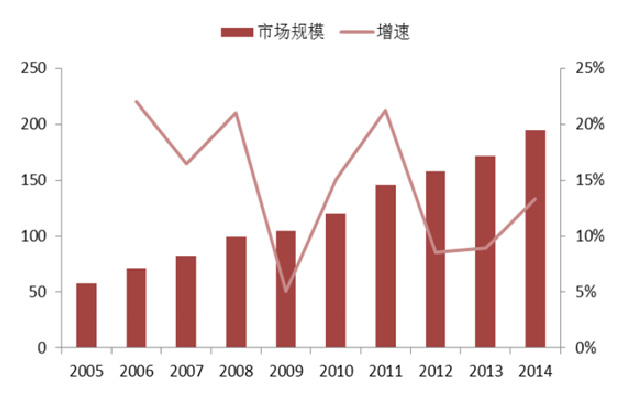

With the development of biotechnology and peptide synthesis technology, more and more peptide drugs have been approved for clinical application. Because of its wide indications, high safety and remarkable curative effect, peptide drugs have been widely used in the prevention, diagnosis and treatment of diseases such as cancer, hepatitis, diabetes and AIDS, and have broad development prospects. At present, the average period of development of peptide drugs is 0.7 years less than that of chemical drugs, and the proportion of drug-based drugs is also higher than that of chemical drugs. The global marketed peptide drugs are increasing year by year, and a large number of peptide drugs have entered clinical research. In recent years, the global peptide drug market compound growth rate is above 12%, higher than the overall drug market, the market size of nearly 20 billion US dollars (as shown below), is expected to reach 25.4 billion US dollars by 2018. The overall size of peptide drugs is still small, but with the maturity of synthetic technology and the development of formulation technology, peptide drugs have a large space for development.

1.2 Status of the domestic market

Compared with foreign developed countries, China's peptide drug industry still has a large gap, and the product structure also has certain differences. At present, the proportion of immuno-enhancement products in China's peptide drug market is relatively large, such as thymopentin, thymus, etc., while anti-tumor, diabetes, rare diseases and other varieties share less, the market is not mature, and there is much room for development. . Compared with the international market, China's peptide drug market is still in a period of rapid growth. On the one hand, due to the immature market of peptide drugs in China, some large varieties such as tumors and diabetes have a small market share and huge room for growth. On the other hand, factors such as increased aging in China, changes in living habits and environmental degradation have made China The rising prevalence of cancer and chronic diseases has increased the demand for medication.

1.3 disparity domestic peptide drugs industry and Analysis

At present, the structural problems affecting the development of the pharmaceutical industry are increasingly prominent, mainly reflected in:

(1) China's pharmaceutical enterprises have serious competition for homogenization, weak innovation capability, lack of independent innovation and high value-added products.

(2) The lack of stamina for sustainable development, the lack of international competitiveness, and the long-term accumulation of structural problems such as serious environmental pollution and high energy consumption have become increasingly prominent.

(3) The industrial concentration is low and the profitability is not strong; the situation of multiple, small, scattered and low has not been completely changed. The scale, industrialization and intensification are not high, and large enterprises account for only 1.83% of the total number of enterprises.

(4) Domestic-funded enterprises account for 80% of the total number of enterprises, and the total profit only accounts for 61.86% of the whole industry. The profitability is significantly lower than that of Hong Kong, Macao and Taiwan and foreign-invested enterprises.

1.4 Opportunities and challenges in the field of peptides

With the aging of the population, the incidence of diseases such as diabetes and cancer is on the rise, and the emergence of multidrug resistance in bacteria is also in need of new anti-infective drugs. The polypeptide drug has a wide range of indications and is suitable for various therapeutic fields such as endocrine and metabolic regulation systems, anti-tumor and anti-infection, and has high specificity and high safety.

Grabbing imitation is already the hottest word in recent years, but most of the imitations are small-molecule drugs, while macromolecular drugs are unattended. The main reason is the technical barriers that are difficult to break through. At present, in the domestic sales of peptides, except glutathione, thymopentin, leuprolide, octreotide can be produced independently, the rest are imported, and imported products account for nearly 80% of the market. At present, the synthesis of peptides in China is still in its infancy, and the products that can be produced independently in China are also short peptides of no more than 10 amino acids.

The research and development of peptide products is different from general chemical drugs. It requires a little accumulation and long-term challenges. If it is still done in the same way as the previous three types of drugs, it is difficult to come up with results. Most of the currently marketed peptides are short peptides of 40 amino acids or less, and biofermentation has no advantage over solid phase synthesis. The difficulty in solid phase synthesis of peptides lies in impurity control and purification production. According to statistics, the probability of approval of peptide drugs entering clinical research is 23%-26%, which is significantly higher than that of small molecule drugs. Therefore, the risk of developing peptide drugs is relatively small. Due to technical conditions and limitations of equipment and equipment, China's peptide drugs are still in their infancy, and there are not many peptide drugs for clinical application, and there is huge room for future development.

Second, antibody-conjugated drugs (ADC)

Antibody-drug conjugates (ADC), a drug that couples a compound drug to a antibody via a linker, thereby reducing the non-specific systemic toxicity of drugs commonly found in chemotherapy. Research and development hotspots for therapeutic monoclonal antibodies. ADCs are transported by blood to identify and recognize surface cancer cells. The antibody part of ADCs is endocytosed into the cancer cells after being bound to the antigen and further cleaved in the lysosome, releasing the killing effect (acting on DNA or cells) Microtubules of compound drugs. After cell death of the ADC drug is lysed, the toxin molecules are released to other nearby tumor cells for further killing. The development of ADCs includes: appropriate drug targets, highly specific antibodies, ideal conjugates, and highly effective drugs.

From the development cycle of antibody technology: ADC antibody drugs will be concentrated in 2016-2020. First, the approval of Kadcyla and Adcetis has proven that ADC technology is maturing. Secondly, according to the history of antibody preparation technology, it takes about 15 years of incubation period for the corresponding drug market. The ADC technology has basically completed the 15-year incubation period since its birth in 2000. Therefore, we judge that the field of ADC antibody drugs will be concentrated in 2016-2020. There are currently more than 30 ADC drugs entering the clinical development phase. However, there are only 4 drugs for solid tumors. Mainly due to the difficulty of antibodies reaching the deep part of the solid tumor through the capillary endothelial layer and through the extracellular space of the tumor.

From the FDA's research varieties: ADC antibody drugs are currently in clinical phase II/III, and it is expected to be approved. At present, ADC antibody drugs are still in the late stage of clinical trials. With the significant efficacy of ADC drugs and the high probability of priority approval, we expect ADC drugs to be approved in the next 2-3 years. Antibody-conjugated drugs are a new growth point for cancer-targeted drugs that are well-deserved. The report shows that the ADC market will develop rapidly in the next 10 years. It is expected that 7-10 ADC drugs will be available by 2024, and the ADC market will reach 10 billion US dollars in 2024. The two ADC drugs currently on the market have shown rapid growth and become the new growth point of targeted drugs. Take Roche's Kadcyla as an example. It went public in 2013 and sold in the first quarter of 2013 to reach $20 million.

From the efficacy of ADC: as an antibody-small molecule drug coupling agent, ADC drugs can significantly improve the survival of tumor patients compared with the direct use of antibody + chemical combination therapy. The ADC drug itself is a good concept, but its technology transformation still expects a bigger breakthrough. As a missile's targeting and small molecules as a warhead of toxic molecules, two key points are already in place, but antibodies need to be effectively internalized, linkers need efficient release, and stability is maintained outside the cell. There are still many difficulties. The proportion of small molecules that enter the target cells and work insignificantly presents a potential problem of great effectiveness and safety.

At present, the most advanced ADC drugs are developed using traditional coupling technology. The biggest disadvantage is that the product is a mixture of different drug molecules per antibody; the specific position of the drug cannot be achieved, and the clinical evaluation data is not uniform. In order to solve this problem, directional coupling technology has become a hot spot for major pharmaceutical companies. Using the directional coupling technique, the same number of drug molecules can be carried on each antibody to obtain a uniform ADC drug, so that a more stable and effective effect can be obtained in the clinic. Another trend is the development of antibody drugs from monovalent drugs to multivalent drugs. It is expected that several synergistic small molecules can be coupled to one antibody to improve the drug's efficacy. This requires a more complete antibody-coupling technique, requiring at least two or more techniques to be adjusted, designing a variety of different coupling groups, and ultimately multi-valent coupling of ADC drugs through Linker's diversification of drug linkages. .

About the Author:

Zhou Yong, founder/Chairman of Gaosheng Biomedicine, co-founder of Gaochuanghui Biomedical Transformation Platform, Vice President of Beijing Haidian District Biological and Health Industry Association, Vice President of Chongqing Pharmaceutical Industry Association, and high-level talents in Chongqing Special support plan candidates, Chongqing innovation and entrepreneurial leading talents.

Longtail tuna,long tail tuna eating quality,longtail tuna eating quality

Zhoushan Boda Aquatic Products Co.,Ltd , https://www.baida-aquatic.com